✨ What is Ind AS 116 / IFRS 16 – Explained Simply

In the past, companies could lease big assets like buildings or machinery and not show them on their balance sheet — this made it hard to see their real financial commitments.

To fix this, Ind AS 116 (in India, from April 1, 2019) and IFRS 16 (globally, from January 1, 2019) were introduced. These new standards made lease accounting more transparent and gave a more realistic picture of a company’s financial health.

🎯 What Changed?

Earlier, companies categorized leases into:

- Operating leases (off balance sheet), and

- Finance leases (on balance sheet).

Under Ind AS 116 / IFRS 16, this distinction is removed for lessees. Now, most lease agreements must be recorded on the balance sheet, just like if the company had bought the asset on a loan.

This means two things:

- You record a Right-of-Use (RoU) asset — the benefit of using the asset.

- You also record a Lease Liability — your obligation to make payments.

This change improves clarity for investors, lenders, and other stakeholders because it shows the true size of the commitments the company has taken on.

📌 Scope of Ind AS 116 – What It Covers and What It Doesn’t

Ind AS 116 covers almost all lease agreements, whether you lease office space, vehicles, equipment, or machinery.

However, there are some exceptions — leases that are not covered under Ind AS 116:

❌ Not Covered by Ind AS 116:

| Excluded Lease Type | What It Means |

| 🚜 Exploration/extraction leases | Leases for mining, oil, natural gas exploration, etc. |

| 🐄 Biological assets | Livestock, plants, crops (covered under Ind AS 41) |

| 🛣️ Service concession arrangements | Public-private partnerships like highways or airports (Ind AS 115) |

| 🎞️ Licenses for intellectual property | Licensing of movies, software, or music |

| 🧠 Certain intangible assets leases | Special licensing arrangements for intangible rights |

So, if your lease is about using a physical asset like land, buildings, or equipment — it’s likely covered under Ind AS 116.

In Simple Words:

If you’re using something for a period and paying for it — and it’s not a service or license — you probably need to account for it under Ind AS 116.

Recognition and Measurement of Leases by Lessees under Ind AS 116 / IFRS 16

📘 Journal Entries for Lessee Accounting under Ind AS 116 / IFRS 16

| Stage | Transaction | Journal Entry | Explanation |

| 1️⃣ Lease commencement | Recognition of Right-of-Use (RoU) Asset and Lease Liability | Dr. Right-of-Use Asset ₹XXXCr. Lease Liability ₹XXX | Present value of lease payments recognized as both an asset and a liability |

| If any lease payment made at/before commencement | Dr. Right-of-Use Asset ₹XXXCr. Bank / Cash ₹XXX | Added to RoU asset as part of its cost | |

| If there are initial direct costs | Dr. Right-of-Use Asset ₹XXXCr. Bank / Payables ₹XXX | Included in cost of RoU asset | |

| Provision for restoration cost (ARO) | Dr. Right-of-Use Asset ₹XXXCr. Provision for Dismantling ₹XXX | Estimated dismantling/restoration cost added to asset and liability recognized | |

| 2️⃣ Monthly / Periodic | Depreciation of RoU asset | Dr. Depreciation Expense ₹XXXCr. Accumulated Depreciation ₹XXX | Based on lease term or useful life, whichever is shorter |

| Interest on lease liability | Dr. Finance Cost ₹XXXCr. Lease Liability ₹XXX | Interest expense accrued using effective interest rate method | |

| Lease payment made | Dr. Lease Liability ₹XXXCr. Bank / Cash ₹XXX | Reduces lease liability | |

| 3️⃣ Year-end or Interim | Short-term / low-value lease (optional expensing) | Dr. Lease Expense ₹XXXCr. Bank / Payables ₹XXX | Applied if exemption chosen; lease payments expensed directly |

| 4️⃣ Adjustment Scenario | Modification in lease term or payments (increase) | Dr. Right-of-Use Asset ₹XXXCr. Lease Liability ₹XXX | Adjustment if lease term extended or payments increased |

| Reduction in scope / lease cancellation | Dr. Lease Liability ₹XXXCr. Right-of-Use Asset ₹XXXDr./Cr. P&L | Reflects decrease in lease scope (e.g., floor area or duration) — may involve profit/loss on change | |

| 5️⃣ End of Lease | Asset fully depreciated, liability settled | No entry (if zero balance remains) | Lease ends when RoU = 0 and Liability = 0 |

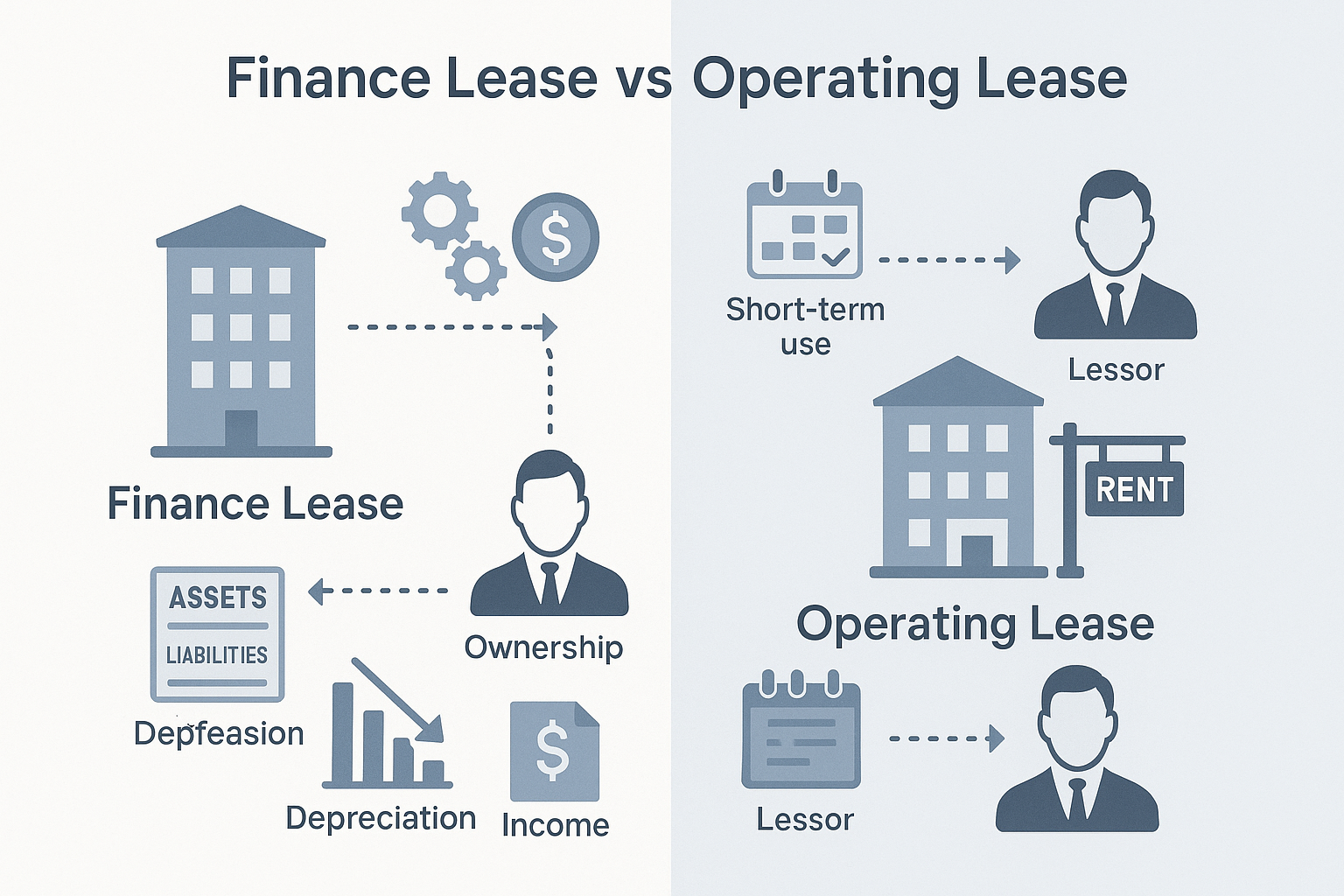

Comparison Table: Finance Lease vs. Operating Lease (Lessor Accounting)

| Criteria | Finance Lease | Operating Lease |

| Ownership | May transfer to lessee at end of lease term | Always retained by the lessor |

| Risk & Reward of Ownership | Transferred to the lessee | Remains with the lessor |

| Asset in Balance Sheet | Removed from lessor’s books; recognized as lease receivable | Remains in lessor’s books |

| Lease Income Recognition | Interest income over lease term (finance income) | Lease rental income on a straight-line or systematic basis |

| Depreciation | Not charged by lessor (lessee accounts for asset) | Charged by lessor, as asset stays in books |

| Type of Payments | Fixed over lease term + possible bargain purchase option | Typically short-term or cancellable leases |

| Indicative Features | – Long term- Non-cancellable- Lessee bears maintenance | – Short term- Cancellable- Lessor bears maintenance |

| Examples | Lease of machinery for 7 years with transfer of ownership | Rental of office space for 2 years with no ownership transfer |

| Accounting by Lessor | Asset replaced with a receivable (net investment in lease) | Asset remains, income and depreciation continue as usual |

| Reporting in Financials | Interest income + Receivable | Lease income + Asset + Depreciation |

🧠 How to Identify a Finance Lease?

A lease is likely to be classified as a finance lease if any one of the following applies:

- Ownership transfers to lessee at the end.

- Lease term covers a major part of the asset’s life.

- Present value of lease payments equals or exceeds substantially all the fair value.

- The asset is so specialized that only the lessee can use it without major modifications.

If none of the above apply, it’s usually classified as an operating lease.

👀 From the Lessee’s View (Post Ind AS 116 / IFRS 16)

Lessees no longer make this distinction. All leases are treated like finance leases, with Right-of-Use asset and Lease Liability on the balance sheet (unless exemptions apply).

Lessor Accounting under Ind AS 116 / IFRS 16

| Type of Lease | Transaction Stage | Journal Entry | Explanation |

| Finance Lease | 📌 At Commencement | Dr. Lease Receivable (Net Investment in Lease) ₹XXXCr. Underlying Asset ₹XXX | Derecognize the leased asset and recognize a receivable equal to the present value of lease payments |

| 🔄 Receipt of Lease Payment | Dr. Bank / Cash ₹XXXCr. Lease Receivable ₹XXX | Cash received reduces the outstanding lease receivable | |

| 💸 Interest Income Accrual | Dr. Lease Receivable ₹XXXCr. Interest Income ₹XXX | Finance income accrued over lease term using effective interest rate method | |

| 📜 End of Lease (optional) | Dr. Asset (if ownership returns) ₹XXXCr. Lease Receivable ₹XXX | If ownership reverts back, asset may be re-recognized (rare under finance lease) | |

| Operating Lease | 🏢 Lease Asset Retained | No entry (asset continues to be recognized) | Asset remains on lessor’s balance sheet and continues to be depreciated |

| 📆 Recognize Lease Income | Dr. Bank / Receivable ₹XXXCr. Lease Income ₹XXX | Recognize rental income on a straight-line basis over lease term (or other systematic basis) | |

| 📉 Depreciation of Asset | Dr. Depreciation Expense ₹XXXCr. Accumulated Depreciation ₹XXX | Depreciate leased asset over its useful life as per standard depreciation policy | |

| 🔄 Maintenance (if any) | Dr. Expense ₹XXXCr. Bank / Payables ₹XXX | Lessor bears maintenance expenses unless transferred to lessee |

🔍 Key Differences: Finance Lease vs Operating Lease (For Lessor)

| Feature | Finance Lease | Operating Lease |

| Asset remains on balance sheet? | ❌ No – Derecognized | ✅ Yes – Retained by lessor |

| Income type | Interest income (finance income) | Lease rental income |

| Receivable recognized? | ✅ Yes – Net investment in lease | ❌ No receivable unless rent unpaid |

| Depreciation by lessor? | ❌ No – Asset is derecognized | ✅ Yes – Regular depreciation |

| Risk and rewards | Transferred to lessee | Retained by lessor |

📢 Disclosure Requirements under Ind AS 116 / IFRS 16

To ensure transparency and consistency, lessees (and to some extent, lessors) must make detailed disclosures in their financial statements. These disclosures help users understand the impact of leases on the financial position, performance, and cash flows of the company.

Here’s a breakdown of what companies are required to disclose:

🧾 1. Breakdown of Lease-related Expenses

Lessees must disclose:

- Depreciation of Right-of-Use (RoU) assets by class of underlying asset (e.g., buildings, vehicles, machinery)

- Interest expense on lease liabilities

- Short-term lease expenses (if exemption taken)

- Low-value asset lease expenses

- Variable lease payments not included in lease liability

📘 This gives insight into how much of lease cost is actual interest vs. asset usage.

💸 2. Total Cash Outflows for Leases

Lessees should present:

- Total cash paid for leases during the period

- This includes fixed and variable payments, short-term lease payments, and payments for low-value leases

📝 Helps users assess the lease-related burden on cash flows.

📆 3. Maturity Analysis of Lease Liabilities

A table must show the undiscounted cash flows (lease payments) due in:

- Year 1

- Years 2–5

- Beyond 5 years

Example format:

| Period | Amount (₹) |

| Within 1 year | ₹50,000 |

| 1–5 years | ₹2,00,000 |

| After 5 years | ₹1,00,000 |

🔎 Investors can use this to understand future obligations.

🧰 4. Practical Expedients and Exemptions Applied

Companies must disclose if they’ve opted for:

- Short-term lease exemption

- Low-value asset exemption

- Not separating lease and non-lease components

✅ This shows whether the company applied any simplification options allowed by the standard.

🎯 Key Judgments Required under Ind AS 116 / IFRS 16

Ind AS 116 is not just a rulebook — it requires significant judgment in several areas. Here are the main decisions management must make:

📑 1. Does the Contract Contain a Lease?

Not all contracts that involve payment for use are leases.

To qualify as a lease:

- There must be an identified asset

- The lessee must have the right to control the use of the asset

🎯 Judgment is needed to distinguish service contracts from leases.

⏳ 2. Determining the Lease Term

Lease term includes:

- The non-cancellable period

- Any extension options the lessee is reasonably certain to exercise

- Less termination options the lessee is likely to exercise

📌 This affects both asset and liability values — over- or underestimating can distort financials.

📉 3. Choosing the Discount Rate

Use either:

- The interest rate implicit in the lease (if known), or

- The lessee’s incremental borrowing rate

🔐 This rate directly affects the size of the lease liability.

⚖️ 4. Separating Lease and Non-Lease Components

Some contracts include both:

- A lease (e.g., rental of machinery)

- And non-lease services (e.g., maintenance, insurance)

Companies must either:

- Separate them and account only for the lease part, or

- Elect not to separate (practical expedient)

📊 This impacts both RoU asset and expense recognition.

Final Tip for Readers

If you’re preparing financial statements under Ind AS 116 / IFRS 16, don’t underestimate the impact of these disclosures and judgments. They not only ensure compliance but also reflect how well you understand and manage your lease obligations.