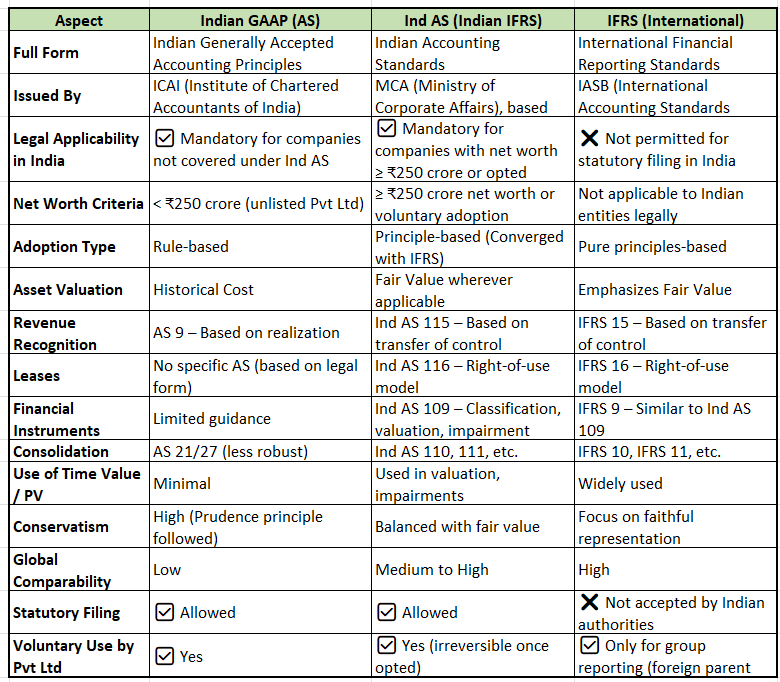

Summary of Comparison Table: Indian GAAP vs Ind AS vs IFRS

In detail

- Indian GAAP (accounting standard)

Regulatory Framework

Private limited companies in India are governed by:

- Companies Act, 2013

- Accounting Standards issued by ICAI (i.e., Indian GAAP or Ind AS depending on applicability)

- Ministry of Corporate Affairs (MCA) notifications

When is Indian GAAP applicable?

Private Limited Company in any industry—whether manufacturing, service, tech, or trading—must follow Indian GAAP only if:

- It is not listed on any stock exchange

- Its net worth is below ₹250 crore

- It has not voluntarily opted for Ind AS

But Ind AS (mandatory) for Net worth ≥ ₹250 crore (if unlisted)

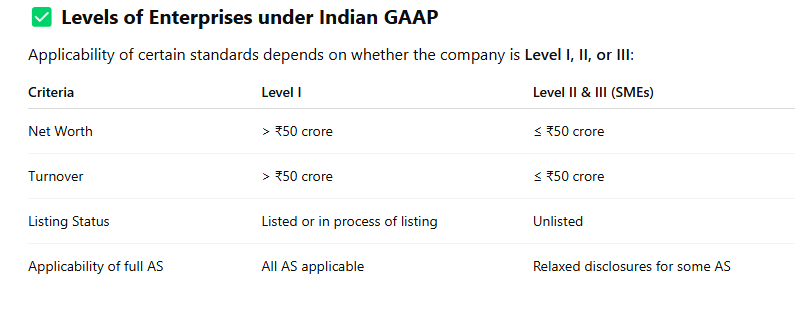

List of Indian Accounting Standards (AS 1 to AS 32)

Note: Not all standards are mandatory for all companies. Some apply only to Level I (larger) companies.

| AS No. | Standard Name | Summary |

| AS 1 | Disclosure of Accounting Policies | Requires disclosure of significant policies used in financial statements. |

| AS 2 | Valuation of Inventories | Prescribes method of valuing inventories at lower of cost or net realizable value. |

| AS 3 | Cash Flow Statements | Requires classification into operating, investing, and financing activities (mandatory for Level I). |

| AS 4 | Contingencies and Events after Balance Sheet Date | Events after the balance sheet that require adjustments/disclosures. |

| AS 5 | Net Profit or Loss for the Period, Prior Period Items & Changes in Accounting Policies | Covers treatment and presentation of extraordinary items and prior period items. |

| AS 6 | Depreciation Accounting (Withdrawn) | Now covered under Schedule II of Companies Act. |

| AS 7 | Construction Contracts | Accounting for long-term contracts using percentage of completion method. |

| AS 9 | Revenue Recognition | When and how to recognize revenue from sale of goods, services, and interest/dividends. |

| AS 10 | Property, Plant, and Equipment | Recognition and accounting for fixed assets, including revaluation. |

| AS 11 | Effects of Changes in Foreign Exchange Rates | Accounting for foreign currency transactions and translation. |

| AS 12 | Government Grants | Recognition of grants related to revenue or capital assets. |

| AS 13 | Accounting for Investments | Classification, valuation, and income recognition from investments. |

| AS 14 | Amalgamations | Accounting for mergers (pooling of interest/purchase method). |

| AS 15 | Employee Benefits | Recognition and disclosure of short-term and long-term employee benefits. |

| AS 16 | Borrowing Costs | Capitalization of interest related to qualifying assets. |

| AS 17 | Segment Reporting | Required for Level I companies. Disclosure of revenue, profit, and assets by segment. |

| AS 18 | Related Party Disclosures | Required disclosure of related party transactions and relationships. |

| AS 19 | Leases | Accounting for finance and operating leases by lessor and lessee. |

| AS 20 | Earnings per Share | Calculation and disclosure of basic and diluted EPS (Level I only). |

| AS 21 | Consolidated Financial Statements | Required for companies with subsidiaries (Level I). |

| AS 22 | Accounting for Taxes on Income | Recognition of deferred tax asset/liability based on timing differences. |

| AS 23 | Accounting for Investments in Associates | Equity method to be used in consolidated financials. |

| AS 24 | Discontinuing Operations | Disclosure and measurement of operations to be discontinued. |

| AS 25 | Interim Financial Reporting | For entities preparing quarterly/half-yearly financials. |

| AS 26 | Intangible Assets | Recognition and amortization of intangible assets. |

| AS 27 | Joint Ventures | Proportionate consolidation or equity method for joint ventures. |

| AS 28 | Impairment of Assets | Assets to be written down if carrying amount exceeds recoverable value. |

| AS 29 | Provisions, Contingent Liabilities & Assets | Recognition and disclosure criteria for provisions and contingent items. |

| AS 30-32 | Financial Instruments (Recommendatory, not mandatory) | Aligns with IFRS 9 but never became fully mandatory under Indian GAAP. |

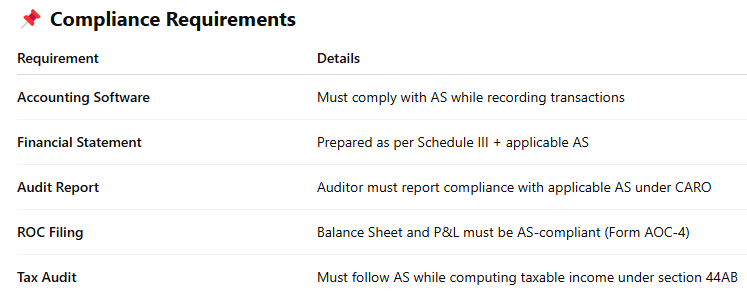

Summary for Private Ltd Companies Using Indian GAAP

- Use AS 1–29 depending on company size and applicability

- Must follow Schedule III of the Companies Act for format

- Can opt voluntarily for Ind AS, but cannot revert back

- Not allowed to use pure IFRS for statutory reporting

- Indian Accounting Standards (Ind AS) for Private Limited Companies

Issued by: Ministry of Corporate Affairs (MCA), based on IFRS

Framework: Principle-based, fair-value-oriented

Legal Basis: Section 133 of the Companies Act, 2013

Applicability:

- Mandatory for companies with net worth ≥ ₹250 crore

- Voluntary for any company; once adopted, irreversible

Full List of Ind AS

| Ind AS No. | Title | Key Purpose |

| Ind AS 1 | Presentation of Financial Statements | Prescribes overall financial statement structure |

| Ind AS 2 | Inventories | Valuation at lower of cost or net realizable value |

| Ind AS 7 | Statement of Cash Flows | Cash flow classification: Operating, Investing, Financing |

| Ind AS 8 | Accounting Policies, Changes in Estimates and Errors | Retrospective application and disclosure |

| Ind AS 10 | Events After Reporting Period | Events that affect financials post year-end |

| Ind AS 12 | Income Taxes | Deferred tax based on balance sheet approach |

| Ind AS 16 | Property, Plant and Equipment | Recognition, depreciation, revaluation of fixed assets |

| Ind AS 19 | Employee Benefits | Accounting for short/long-term and post-employment benefits |

| Ind AS 20 | Government Grants | Recognition of subsidies and grants |

| Ind AS 21 | Effects of Changes in Foreign Exchange Rates | Treatment of foreign transactions and balances |

| Ind AS 23 | Borrowing Costs | Capitalization of borrowing cost related to qualifying assets |

| Ind AS 24 | Related Party Disclosures | Disclosure of relationships and transactions |

| Ind AS 27 | Separate Financial Statements | Reporting for parent or investment companies |

| Ind AS 28 | Investments in Associates and Joint Ventures | Equity method accounting |

| Ind AS 32 | Financial Instruments: Presentation | Classification as equity or liability |

| Ind AS 33 | Earnings per Share | Computation and disclosure of EPS |

| Ind AS 34 | Interim Financial Reporting | Format and disclosures for quarterly statements |

| Ind AS 36 | Impairment of Assets | Recoverable amount vs. carrying value |

| Ind AS 37 | Provisions, Contingent Liabilities and Contingent Assets | Recognition and disclosure of obligations |

| Ind AS 38 | Intangible Assets | Recognition and amortization of intangibles |

| Ind AS 40 | Investment Property | Recognition of property held for rental/investment purposes |

| Ind AS 41 | Agriculture | Biological assets and agricultural produce |

| Ind AS 101 | First-time Adoption of Ind AS | Transition rules from Indian GAAP to Ind AS |

| Ind AS 102 | Share-based Payment | Treatment of ESOPs and other equity-settled instruments |

| Ind AS 103 | Business Combinations | Merger vs. acquisition accounting (Purchase method) |

| Ind AS 104 | Insurance Contracts | (Limited applicability) |

| Ind AS 105 | Non-Current Assets Held for Sale and Discontinued Operations | Classification and separate disclosure |

| Ind AS 106 | Exploration for and Evaluation of Mineral Resources | Industry-specific |

| Ind AS 107 | Financial Instruments: Disclosures | Risk disclosures (credit, liquidity, market) |

| Ind AS 108 | Operating Segments | Segment-wise financial reporting |

| Ind AS 109 | Financial Instruments | Classification, measurement, impairment |

| Ind AS 110 | Consolidated Financial Statements | Control-based consolidation |

| Ind AS 111 | Joint Arrangements | Classification into joint operations and joint ventures |

| Ind AS 112 | Disclosure of Interests in Other Entities | Structured entities, associates, etc. |

| Ind AS 113 | Fair Value Measurement | Hierarchy and principles of fair valuation |

| Ind AS 114 | Regulatory Deferral Accounts | Industry-specific (power/utilities) |

| Ind AS 115 | Revenue from Contracts with Customers | 5-step model based on control transfer |

| Ind AS 116 | Leases | Right-of-use model (for lessee) |

Reporting under Ind AS

| Report Component | Requirement under Ind AS |

| Balance Sheet | As per Schedule III (Div II) + Ind AS disclosures |

| Statement of P&L | Includes OCI (Other Comprehensive Income) |

| Cash Flow Statement | Ind AS 7: Mandatory (Indirect method) |

| Statement of Changes in Equity | Mandatory under Ind AS 1 |

| Notes to Accounts | Extensive disclosures, especially for financial instruments, leases, segments, etc. |

Let’s understand key differences b/w AS(GAAP) and Ind AS(IFRS)-

Whether a company follows Accounting Standards (AS) or Indian Accounting Standards (Ind AS) depends on its legal structure, listing status, and financial thresholds such as net worth.

| Topic | Ind AS (No. & Title) | AS (No. & Title) | Key Differences |

| Financial Statements | Ind AS 1 – Presentation of Financial Statements | AS 1 – Disclosure of Accounting Policies | Ind AS includes full structure, OCI, equity statement. AS is limited to policy disclosure. |

| Inventories | Ind AS 2 – Inventories | AS 2 – Valuation of Inventories | Both are similar, but Ind AS emphasizes NRV based on IFRS. |

| Cash Flow Statement | Ind AS 7 – Statement of Cash Flows | AS 3 – Cash Flow Statements | Ind AS allows only indirect method for operating cash flows. |

| Accounting Policies/Errors | Ind AS 8 – Accounting Policies, Estimates and Errors | AS 5 – Net Profit or Loss, Prior Period Items | Ind AS requires retrospective restatement. AS treats prior items separately. |

| Events after Balance Sheet | Ind AS 10 – Events after Reporting Period | AS 4 – Contingencies and Events after B/S Date | AS includes contingencies; Ind AS deals only with post-reporting events. |

| Income Taxes | Ind AS 12 – Income Taxes | AS 22 – Taxes on Income | Ind AS uses balance sheet approach; AS uses income statement approach. |

| PPE (Fixed Assets) | Ind AS 16 – Property, Plant & Equipment | AS 10 – Accounting for Fixed Assets | Ind AS allows revaluation model and component accounting. AS follows cost model only. |

| Employee Benefits | Ind AS 19 – Employee Benefits | AS 15 – Employee Benefits | Ind AS is more detailed; includes actuarial assumptions and discount rates. |

| Govt. Grants | Ind AS 20 – Government Grants | AS 12 – Government Grants | Ind AS based on IFRS model; AS includes capital/revenue grants. |

| Foreign Exchange | Ind AS 21 – Effects of Foreign Exchange Rates | AS 11 – The Effects of Changes in FX Rates | Ind AS requires fair value for FX derivatives; AS allows capitalization in certain cases. |

| Borrowing Costs | Ind AS 23 – Borrowing Costs | AS 16 – Borrowing Costs | Similar treatment; Ind AS includes broader qualifying assets. |

| Related Party | Ind AS 24 – Related Party Disclosures | AS 18 – Related Party Disclosures | Ind AS has broader definition and deeper disclosure requirements. |

| Separate Financials | Ind AS 27 – Separate Financial Statements | No equivalent | Ind AS provides guidance on standalone investment accounting. |

| Associates & JVs | Ind AS 28 – Investments in Associates and Joint Ventures | AS 23 – Accounting for Investments in Associates | Ind AS requires equity method; AS allows cost method. |

| Financial Instruments (Pres.) | Ind AS 32 – Financial Instruments: Presentation | No equivalent | Ind AS classifies debt vs equity based on substance. |

| EPS | Ind AS 33 – Earnings per Share | AS 20 – Earnings per Share | Largely aligned; Ind AS includes potential shares & OCI impact. |

| Interim Reporting | Ind AS 34 – Interim Financial Reporting | AS 25 – Interim Financial Reporting | Ind AS requires condensed FS with full disclosures. |

| Impairment of Assets | Ind AS 36 – Impairment of Assets | AS 28 – Impairment of Assets | Ind AS uses discounted cash flow (value in use); AS does not. |

| Provisions | Ind AS 37 – Provisions, Contingent Liabilities and Assets | AS 29 – Provisions, Contingent Liabilities | Similar, but Ind AS is stricter on recognition. |

| Intangible Assets | Ind AS 38 – Intangible Assets | AS 26 – Intangible Assets | Ind AS allows revaluation model; AS allows only cost model. |

| Investment Property | Ind AS 40 – Investment Property | AS 13 – Investments (indirectly) | Ind AS has a separate standard; AS treats it as long-term investment. |

| Agriculture | Ind AS 41 – Agriculture | No equivalent | Ind AS introduces fair value for biological assets. |

| First-time Adoption | Ind AS 101 – First-time Adoption of Ind AS | No equivalent | Provides exemptions and optional treatments. |

| Share-based Payment | Ind AS 102 – Share-based Payment | No equivalent | Covers ESOPs, stock-based compensation. |

| Business Combinations | Ind AS 103 – Business Combinations | AS 14 – Amalgamation | Ind AS uses acquisition method only; AS allows pooling of interest. |

| Discontinued Operations | Ind AS 105 – Non-current Assets Held for Sale | AS 24 – Discontinuing Operations | Ind AS is aligned with IFRS and more detailed. |

| Operating Segments | Ind AS 108 – Operating Segments | AS 17 – Segment Reporting | Ind AS based on internal reporting; AS is based on business/geography. |

| Financial Instruments | Ind AS 109 – Financial Instruments | AS 30/31/32 (not mandatory) | Ind AS mandatory for all; includes classification, impairment, hedging. |

| Consolidated FS | Ind AS 110 – Consolidated Financial Statements | AS 21 – Consolidated Financial Statements | Ind AS uses control definition; AS uses ownership %. |

| Joint Arrangements | Ind AS 111 – Joint Arrangements | AS 27 – Joint Ventures | Ind AS classifies as operations or ventures; AS uses proportionate consolidation. |

| Disclosure in Entities | Ind AS 112 – Disclosure of Interests in Other Entities | Covered in AS 21–27 collectively | Ind AS combines all entity disclosures in one place. |

| Fair Value Measurement | Ind AS 113 – Fair Value Measurement | No equivalent | Ind AS defines fair value hierarchy and measurement basis. |

| Revenue Recognition | Ind AS 115 – Revenue from Contracts with Customers | AS 9 – Revenue Recognition | Ind AS uses a 5-step model; AS uses basic performance criteria. |

| Leases | Ind AS 116 – Leases | AS 19 – Leases | Ind AS brings operating leases on the balance sheet for lessees. |

Final Conclusion:-

- Once a company adopts Ind AS, it cannot revert to AS.

- Ind AS is mandatory for:

- All listed companies

- All unlisted companies with net worth ≥ ₹250 crore

- Their holding, subsidiary, associate, and joint venture companies

- AS is followed by:

- Unlisted companies with net worth < ₹250 crore

- SMEs and private companies not meeting Ind AS thresholds

- Non-corporate entities (on a voluntary or recommended basis)